To Get More Information on Industrial Control & Factory Automation Market - Request Sample Report

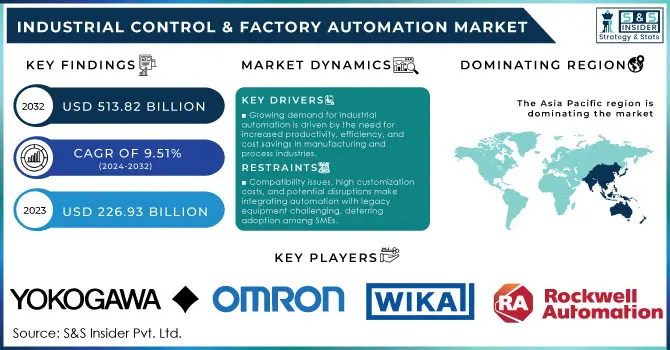

The Industrial Control & Factory Automation Market Size was valued at USD 226.93 Billion in 2023 and is now anticipated to grow to USD 513.82 Billion by 2032, displaying a compound annual growth rate (CAGR) of 9.51% during the forecast Period 2024-2032.

The Industrial Control and Factory Automation Market is undergoing significant transformation, driven by rapid technological advancements and a growing emphasis on operational efficiency and sustainability. As of 2023, an estimated 75 billion devices are expected to be connected to the Internet of Things (IoT), profoundly impacting industrial operations. The integration of IoT technologies enables real-time data collection and analysis, allowing manufacturers to monitor performance, predict maintenance needs, and make informed decisions. This connectivity leads to smarter factories that can operate autonomously, enhancing operational efficiency by up to 30% and significantly reducing downtime.

In addition to IoT, there is a strong focus on energy efficiency within industrial automation. The International Energy Agency (IEA) suggests that implementing automation solutions can result in energy savings of 20% to 30%, promoting sustainability and lowering operational costs. The adoption of artificial intelligence (AI) and machine learning (ML) technologies is also gaining momentum, with around 40% of companies planning to implement AI-driven solutions in their manufacturing processes within the next two years. These technologies facilitate predictive maintenance, potentially reducing maintenance costs by up to 25% and extending the lifespan of critical assets. Collaborative robots (cobots) are another vital aspect of this evolving landscape, projected to exceed USD 4 billion. Cobots are designed to work alongside human operators, improving efficiency in tasks that require both human dexterity and robotic precision.

| Type of Automation System | Description | Commercial Products |

|---|---|---|

| Programmable Logic Controllers (PLC) | Industrial computers used to control machinery and processes, enabling real-time control. | Siemens SIMATIC S7, Rockwell ControlLogix |

| Distributed Control System (DCS) | Systems that manage large processes across multiple control points in real-time. | ABB System 800xA, Honeywell Experion PKS |

| Supervisory Control and Data Acquisition (SCADA) | Systems for monitoring and controlling industrial processes remotely. | Schneider Electric EcoStruxure, GE iFIX |

| Human Machine Interface (HMI) | Interfaces that allow human operators to interact with the system for monitoring and control. | Allen-Bradley PanelView, Siemens WinCC |

| Industrial Internet of Things (IIoT) | Devices and sensors networked for data exchange, enabling predictive maintenance and analytics. | PTC ThingWorx, Bosch Rexroth IoT Gateway |

| Machine Vision Systems | Cameras and software used for automated inspection and quality control. | Cognex In-Sight, Keyence CV-X Series |

| Motion Control Systems | Systems for precise control of machinery movement, used in robotics and CNC machinery. | Siemens Sinamics, Mitsubishi MR-J4 |

| Robotics | Automated robots for handling, assembling, and packing in manufacturing processes. | Fanuc LR Mate, ABB IRB 6700 |

| Industrial Safety Systems | Safety mechanisms to protect workers and equipment, such as emergency shutdowns. | Honeywell Safety Manager, Rockwell GuardLogix |

| Process Automation | Technologies to automate manufacturing processes for efficiency and reduced human intervention. | Emerson DeltaV, Yokogawa CENTUM VP |

DRIVERS

The demand for industrial automation has surged as industries strive for enhanced productivity, efficiency, and cost-effectiveness. Automation technologies, encompassing robotics, AI-driven systems, and IoT-enabled devices, enable industries to streamline processes, reduce human error, and improve product quality. Manufacturing and process sectors, in particular, have rapidly adopted these technologies to maintain competitiveness and meet rising consumer demands. In recent years, labor shortages and rising operational costs have further accelerated automation adoption, as automated systems can operate continuously, reducing dependency on human labor and cutting down costs associated with workforce management. In the manufacturing sector, automation can increase production speeds by up to 30% and reduce waste by up to 20% through precision and optimized resource usage. In addition, automated systems often bring a return on investment (ROI) within a few years, with studies showing up to 25% cost savings in operational expenses when integrated effectively. According to the research over 70% are investing in automation technologies to improve operational efficiencies and adapt to market changes. Industries ranging from automotive to pharmaceuticals are now deploying automation solutions for tasks that require precision and consistency, such as assembly, packaging, and quality inspection. This trend is not only enhancing productivity but also reducing the production cycle times by nearly 40% in certain sectors, enabling faster delivery and better scalability. As industries embrace automation to address production challenges, the demand for industrial automation systems continues to grow, shaping the future of manufacturing and process sectors globally.

The integration of Artificial Intelligence (AI) and the Internet of Things (IoT) into industrial automation systems has significantly transformed operational efficiency and intelligence. AI-powered analytics and IoT-connected devices allow for real-time data collection, monitoring, and analysis across manufacturing floors, which enhances both productivity and decision-making processes. Predictive maintenance, made possible by this integration, reduces unexpected equipment failures by analyzing data patterns and predicting potential malfunctions before they occur. IoT sensors can continuously monitor machinery performance and detect even subtle changes in vibration, temperature, or other critical metrics. This information, powered by AI algorithms, enables maintenance teams to intervene proactively, reducing downtime by up to 30%.

The adoption of IoT in industrial applications is already substantial, with over 80% of companies expected to incorporate IoT into their automation processes by 2025. Additionally, AI’s role in improving operational decision-making has led to the development of autonomous production lines, where machines can adjust parameters based on real-time data, reducing human error and optimizing resource usage. Studies indicate that smart factories utilizing AI and IoT can achieve up to a 40% increase in operational efficiency compared to traditional setups. As industries strive for digital transformation, these technologies are essential enablers, providing the connectivity and intelligence needed to meet growing demands for precision, speed, and sustainability in modern manufacturing.

RESTRAIN

Integrating automation systems with existing legacy equipment presents significant challenges in the industrial control and factory automation market. Many factories and plants still operate using older machinery and outdated control systems that aren’t readily compatible with modern automation technologies. Connecting these legacy systems to advanced automation platforms, such as those incorporating the Industrial Internet of Things (IIoT) or AI-driven systems, requires extensive customization. This complexity increases implementation time and costs, as businesses often need specialized technicians and engineers to manage compatibility issues, adapt hardware interfaces, and configure software protocols for seamless operation. According to the research by IoT Analytics, around 53% of manufacturers cite compatibility with existing systems as a major hurdle in adopting IIoT and automation solutions.

Additionally, the integration process can disrupt ongoing operations, further adding to costs due to downtime or decreased productivity during the transition. According to research spending approximately 20% to 30% more on such integration projects than anticipated, reflecting unforeseen challenges and the need for custom solutions. These factors can deter especially small and medium-sized enterprises (SMEs) that lack the financial resources to undertake such capital-intensive modifications. Furthermore, the high cost of integration can delay a return on investment, reducing the overall appeal of adopting automation solutions. Consequently, this complexity often slows down the growth of the industrial control and factory automation market, as companies grapple with balancing the benefits of automation against the financial and logistical demands of integration with legacy equipment.

By Solution

Distributed Control Systems (DCS) segment dominated the market share over 36.02% in 2023, due to the widespread adoption of Industrial IoT (IIoT) technologies. This large-scale adoption reflects industrialists’ growing preference for DCS in automated control systems, which provide centralized control with distributed data processing capabilities. DCS systems are vital for sectors like manufacturing and energy, where real-time data from sensors and actuators enables precise operational control and reduces downtime. The ongoing rollout of 5G further amplifies the benefits of IIoT and DCS, especially in high-demand sectors such as power. With the high-speed, low-latency advantages of 5G networks, IIoT integration with DCS has become even more efficient, enabling faster data transfer, enhanced connectivity, and improved operational efficiency.

By Industry

The discrete industry segment dominated the market share over 54.38% in 2023. This industry encompasses the production of tangible goods that are distinct and identifiable, such as nuts, bolts, brackets, assemblies, cables, automobiles, toys, furniture, and smartphones. These products are typically produced in units and can be easily counted or measured, making them crucial for various sectors. At the end of their life cycle, discrete products can often be disassembled and recycled, allowing for sustainable practices in manufacturing and waste management. This capability not only contributes to resource conservation but also enhances the industry's adaptability to changing consumer demands and environmental regulations.

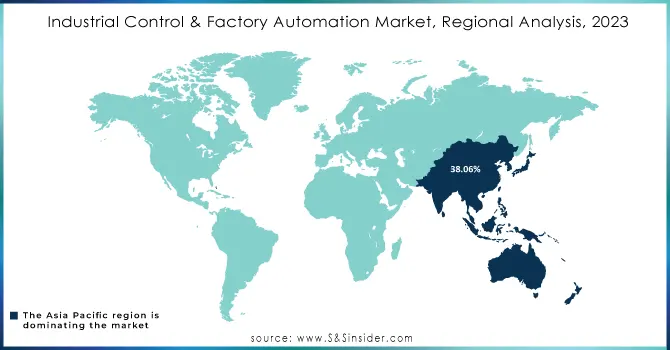

The Asia Pacific region has dominated the market share over 38.06% in 2023. This growth can be attributed to the presence of numerous key market players and a surge in emerging companies across the region. Countries like India and China are witnessing an escalating demand for advanced solutions to optimize industrial plant management, which significantly boosts market growth. The transition from traditional to smart production facilities is becoming increasingly common, fostering greater acceptance of industrial automation technologies. China’s manufacturing sector has seen substantial investments in automation, driven by government initiatives aimed at enhancing productivity and efficiency. Furthermore, the emphasis on Industry 4.0 principles is steering industries toward digitization and connectivity, which collectively enhances the adoption of innovative automation solutions in the region.

North America is witnessing rapid growth in the Industrial Control & Factory Automation Market, primarily due to significant technological advances and the ongoing digital transformation across various sectors. The region's manufacturing units are increasingly adopting state-of-the-art automation technologies to enhance efficiency and streamline business processes. According to the research that 77% of manufacturers in North America believe that digital transformation is essential for staying competitive in the market. Additionally, 50% of manufacturing executives reported investing in advanced technologies like AI, IoT, and robotics to meet rising end-user demands and improve operational efficiency. This drive to embrace innovation is fueled by heightened competition, pushing companies to enhance productivity and reduce costs.

Do You Need any Customization Research on Industrial Control & Factory Automation Market - Inquire Now

Some of the major key players of Industrial Control & Factory Automation Market

Yokogawa Electric Corporation (Control Systems, Field Instruments)

Omron Corporation (Programmable Logic Controllers, Sensors)

WIKA (Pressure Transmitters, Level Sensors)

Mitsubishi Electric Corporation (Industrial Robots, Automation Control Systems)

Rockwell Automation (ControlLogix, FactoryTalk)

Yaskawa Electric Corporation (Servo Drives, Motion Controllers)

Toshiba Corporation (Programmable Logic Controllers, Industrial PCs)

Honeywell International Inc. (Distributed Control Systems, Safety Instrumented Systems)

Dwyer Instruments (Pressure Gauges, Flow Meters)

Stratasys (3D Printers, Additive Manufacturing Solutions)

Hitachi (Industrial Automation Solutions, Control Systems)

Siemens AG (SIMATIC PLCs, SINUMERIK CNC Systems)

Schneider Electric (EcoStruxure, Modicon PLCs)

ABB Ltd. (Industrial Robots, Control Systems)

GE Automation & Controls (iFIX, Proficy Software)

Emerson Electric Co. (DeltaV, Ovation)

KUKA AG (Industrial Robots, Automation Solutions)

FANUC Corporation (Robotic Automation, CNC Systems)

Panasonic Corporation (Automation Solutions, Industrial Robotics)

Advantech (Embedded Automation Computers, Industrial IoT Solutions)

Suppliers for Specializes in energy management and automation, offering EcoStruxure architecture and various control systems of Industrial Control & Factory Automation Market:

Siemens AG

Rockwell Automation, Inc.

ABB Ltd.

Schneider Electric

Mitsubishi Electric Corporation

Honeywell International Inc.

Emerson Electric Co.

Yokogawa Electric Corporation

Omron Corporation

GE Digital (General Electric)

In July 2024: Mitsubishi Electric Corporation announced the signing of a Memorandum of Understanding (MOU) with Thailand's Forth EMS Public Company Limited to explore potential collaboration in co-manufacturing Mitsubishi Electric's Transmit/Receive Modules, intended for use in the Air Surveillance Radar Systems produced by Mitsubishi Electric.

In June 2024: ABB Robotics introduced OmniCore, an advanced automation platform designed to enhance speed, precision, and sustainability. This platform aims to empower businesses and prepare them for future challenges.

In March 2024: Rockwell Automation unveiled the Allen Bradley ArmorBlock 5000 IO-Link master blocks, a new control device that optimizes operations, shortens deployment times, and enhances functionality in demanding industrial environments. These improvements significantly boost the versatility, efficiency, and productivity of premier integrations, facilitating easier automation and maintenance.

In November 2023: NovaTech Automation finalized its acquisition of the product line from TestSwitch LLC. This moves enhanced NovaTech Automation's standing in the industry and broadened its product offerings to include TestSwitch's premier product, the W3TS Test Switch.

In November 2023: Huizenga Automation Group successfully acquired GSE Automation, which provides a diverse array of services such as process development, FEA analysis, and system design. This acquisition was intended to bolster Huizenga's presence in the industrial automation sector, leveraging GSE's extensive expertise to enhance their existing portfolio.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 226.93 Billion |

| Market Size by 2032 | USD 513.82 Billion |

| CAGR | CAGR of 9.51% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component Type (Industrial Robots, Collaborative Industrial Robots, Machine Vision, Control Valves, Field Instruments, Human–Machine Interface (HMI), Industrial PC, Sensors) • By Solution (SCADA, PLC, DCS, MES, Industrial Safety Solutions, PAM) • By Industry, Process Industry ( Oil & Gas, Chemical, Pulp & Paper, Pharmaceutical, Metals & Mining, Food & Beverages, Energy & Power) Discrete Industry (Automotive, Machine Manufacturing, Semiconductor & Electronics, Aerospace & Defense, Medical Device) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Yokogawa Electric Corporation, Omron Corporation, WIKA, Mitsubishi Electric Corporation, Rockwell Automation, Yaskawa Electric Corporation, Toshiba Corporation, Honeywell International Inc., Dwyer Instruments, Stratasys, Hitachi, Siemens AG, Schneider Electric, ABB Ltd., GE Automation & Controls, Emerson Electric Co., KUKA AG, FANUC Corporation, Panasonic Corporation, Advantech. |

| Key Drivers | • Growing demand for industrial automation is driven by the need for increased productivity, efficiency, and cost savings in manufacturing and process industries. • Integrating AI and IoT in automation enhances data analysis and predictive maintenance, driving smarter, digitally transformed industrial operations. |

| RESTRAINTS | • Integrating automation systems with legacy equipment poses significant challenges due to compatibility issues, high customization costs, and potential operational disruptions, which can deter adoption, particularly among small and medium-sized enterprises. |

Ans: The Industrial Control & Factory Automation Market is expected to grow at a CAGR of 9.51% during 2024-2032.

Ans: The Industrial Control & Factory Automation Market was USD 226.93 Billion in 2023 and is expected to Reach USD 513.82 Billion by 2032.

Ans: Growing demand for industrial automation is driven by the need for increased productivity, efficiency, and cost savings in manufacturing and process industries.

Ans: The “Distributed Control Systems (DCS)” segment dominated the Industrial Control & Factory Automation Market.

Ans: Asia-Pacific dominated the Industrial Control & Factory Automation Market in 2023.

TABLE OF CONTENTS

1. Introduction

1.1 Market Definition

1.2 Scope (Inclusion and Exclusions)

1.3 Research Assumptions

2. Executive Summary

2.1 Market Overview

2.2 Regional Synopsis

2.3 Competitive Summary

3. Research Methodology

3.1 Top-Down Approach

3.2 Bottom-up Approach

3.3. Data Validation

3.4 Primary Interviews

4. Market Dynamics

4.1 Market Analysis

4.1.1 Drivers

4.1.2 Restraints

4.1.3 Opportunities

4.1.4 Challenges

4.2 PESTLE Analysis

4.3 Porter’s Five Forces Model

5. Statistical Insights and Trends Reporting

5.1 Manufacturing Output, by region, (2020-2023)

5.2 Utilization Rates, by region, (2020-2023)

5.3 Maintenance and Downtime Metrix

5.4 Technological Adoption Rates, by region

5.5 Export/Import Data, by region (2023)

6. Competitive Landscape

6.1 List of Major Companies, By Region

6.2 Market Share Analysis, By Region

6.3 Product Benchmarking

6.3.1 Product specifications and features

6.3.2 Pricing

6.4 Strategic Initiatives

6.4.1 Marketing and promotional activities

6.4.2 Distribution and Supply Chain Strategies

6.4.3 Expansion plans and new product launches

6.4.4 Strategic partnerships and collaborations

6.5 Technological Advancements

6.6 Market Positioning and Branding

7. Industrial Control & Factory Automation Market Segmentation, By Component Type Type

7.1 Chapter Overview

7.2 Industrial Robots

7.2.1 Industrial Robots Market Trends Analysis (2020-2032)

7.2.2 Industrial Robots Market Size Estimates and Forecasts to 2032 (USD Billion)

7.3 Collaborative Industrial Robots

7.3.1 Collaborative Industrial Robots Market Trends Analysis (2020-2032)

7.3.2 Collaborative Industrial Robots Market Size Estimates and Forecasts to 2032 (USD Billion)

7.4 Machine Vision

7.4.1 Machine Vision Market Trends Analysis (2020-2032)

7.4.2 Machine Vision Market Size Estimates and Forecasts to 2032 (USD Billion)

7.5 Control Valves

7.5.1 Control Valves Market Trends Analysis (2020-2032)

7.5.2 Control Valves Market Size Estimates and Forecasts to 2032 (USD Billion)

7.6 Field Instruments

7.6.1 Field Instruments Market Trends Analysis (2020-2032)

7.6.2 Field Instruments Market Size Estimates and Forecasts to 2032 (USD Billion)

7.7 Human–Machine Interface (HMI)

7.7.1 Human–Machine Interface (HMI) Market Trends Analysis (2020-2032)

7.7.2 Human–Machine Interface (HMI) Market Size Estimates and Forecasts to 2032 (USD Billion)

7.8 Industrial PC

7.8.1 Industrial PC Market Trends Analysis (2020-2032)

7.8.2 Industrial PC Market Size Estimates and Forecasts to 2032 (USD Billion)

7.9 Sensors

7.9.1 Sensors Market Trends Analysis (2020-2032)

7.9.2 Sensors Market Size Estimates and Forecasts to 2032 (USD Billion)

8. Industrial Control & Factory Automation Market Segmentation, By Solution

8.1 Chapter Overview

8.2 SCADA

8.2.1 SCADA Market Trends Analysis (2020-2032)

8.2.2 SCADA Market Size Estimates and Forecasts to 2032 (USD Billion)

8.3 PLC

8.3.1 PLC Market Trends Analysis (2020-2032)

8.3.2 PLC Market Size Estimates and Forecasts to 2032 (USD Billion)

8.4 DCS

8.4.1 DCS Market Trends Analysis (2020-2032)

8.4.2 DCS Market Size Estimates and Forecasts to 2032 (USD Billion)

8.5 MES

8.5.1 MES Market Trends Analysis (2020-2032)

8.5.2 MES Market Size Estimates and Forecasts to 2032 (USD Billion)

8.6 Industrial Safety

8.6.1 Industrial Safety Market Trends Analysis (2020-2032)

8.6.2 Industrial Safety Market Size Estimates and Forecasts to 2032 (USD Billion)

8.7 PAM

8.7.1 PAM Market Trends Analysis (2020-2032)

8.7.2 PAM Market Size Estimates and Forecasts to 2032 (USD Billion)

9. Industrial Control & Factory Automation Market Segmentation, By Industry

9.1 Chapter Overview

9.2 Process Industry

9.2.1 Process Industry Market Trends Analysis (2020-2032)

9.2.2 Process Industry Market Size Estimates and Forecasts to 2032 (USD Billion)

9.2.3 Oil & GAS

9.2.3.1 Oil & GAS Market Trends Analysis (2020-2032)

9.2.3.2 Oil & GAS Market Size Estimates and Forecasts to 2032 (USD Billion)

9.2.4 Chemical

9.2.4.1 Chemical Market Trends Analysis (2020-2032)

9.2.4.2 Chemical Market Size Estimates and Forecasts to 2032 (USD Billion)

9.2.5 Pulp & Paper

9.2.5.1 Pulp & Paper Market Trends Analysis (2020-2032)

9.2.5.2 Pulp & Paper Market Size Estimates and Forecasts to 2032 (USD Billion)

9.2.6 Pharmaceutical

9.2.6.1 Pharmaceutical Market Trends Analysis (2020-2032)

9.2.6.2 Pharmaceutical Market Size Estimates and Forecasts to 2032 (USD Billion)

9.2.7 Metals & mining

9.2.7.1 Metals & mining Market Trends Analysis (2020-2032)

9.2.7.2 Metals & mining Market Size Estimates and Forecasts to 2032 (USD Billion)

9.2.8 Food & Beverages

9.2.8.1 Food & Beverages Market Trends Analysis (2020-2032)

9.2.8.2 Food & Beverages Market Size Estimates and Forecasts to 2032 (USD Billion)

9.2.9 Energy & Power

9.2.9.1 Energy & Power Market Trends Analysis (2020-2032)

9.2.9.2 Energy & Power Market Size Estimates and Forecasts to 2032 (USD Billion)

9.3 Discrete Industry

9.3.1 Discrete Industry Market Trends Analysis (2020-2032)

9.3.2 Discrete Industry Market Size Estimates and Forecasts to 2032 (USD Billion)

9.3.3 Automotive

9.3.3.1 Automotive Market Trends Analysis (2020-2032)

9.3.3.2 Automotive Market Size Estimates and Forecasts to 2032 (USD Billion)

9.3.4 Machine manufacturing

9.3.4.1 Machine manufacturing Market Trends Analysis (2020-2032)

9.3.4.2 Machine manufacturing Market Size Estimates and Forecasts to 2032 (USD Billion)

9.3.5 Semiconductor & Electronics

9.3.5.1 Semiconductor & Electronics Market Trends Analysis (2020-2032)

9.3.5.2 Semiconductor & Electronics Market Size Estimates and Forecasts to 2032 (USD Billion)

9.3.6 Aerospace & Defense

9.3.6.1 Aerospace & Defense Market Trends Analysis (2020-2032)

9.3.6.2 Aerospace & Defense Market Size Estimates and Forecasts to 2032 (USD Billion)

9.3.7 Medical device

9.3.7.1 Medical device Market Trends Analysis (2020-2032)

9.3.7.2 Medical device Market Size Estimates and Forecasts to 2032 (USD Billion)

10. Regional Analysis

10.1 Chapter Overview

10.2 North America

10.2.1 Trends Analysis

10.2.2 North America Industrial Control & Factory Automation Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

10.2.3 North America Industrial Control & Factory Automation Market Estimates and Forecasts, By Component Type (2020-2032) (USD Billion)

10.2.4 North America Industrial Control & Factory Automation Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

10.2.5 North America Industrial Control & Factory Automation Market Estimates and Forecasts, By Industry (2020-2032) (USD Billion)

10.2.6 USA

10.2.6.1 USA Industrial Control & Factory Automation Market Estimates and Forecasts, By Component Type (2020-2032) (USD Billion)

10.2.6.2 USA Industrial Control & Factory Automation Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

10.2.6.3 USA Industrial Control & Factory Automation Market Estimates and Forecasts, By Industry (2020-2032) (USD Billion)

10.2.7 Canada

10.2.7.1 Canada Industrial Control & Factory Automation Market Estimates and Forecasts, By Component Type (2020-2032) (USD Billion)

10.2.7.2 Canada Industrial Control & Factory Automation Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

10.2.7.3 Canada Industrial Control & Factory Automation Market Estimates and Forecasts, By Industry (2020-2032) (USD Billion)

10.2.8 Mexico

10.2.8.1 Mexico Industrial Control & Factory Automation Market Estimates and Forecasts, By Component Type (2020-2032) (USD Billion)

10.2.8.2 Mexico Industrial Control & Factory Automation Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

10.2.8.3 Mexico Industrial Control & Factory Automation Market Estimates and Forecasts, By Industry (2020-2032) (USD Billion)

10.3 Europe

10.3.1 Eastern Europe

10.3.1.1 Trends Analysis

10.3.1.2 Eastern Europe Industrial Control & Factory Automation Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

10.3.1.3 Eastern Europe Industrial Control & Factory Automation Market Estimates and Forecasts, By Component Type (2020-2032) (USD Billion)

10.3.1.4 Eastern Europe Industrial Control & Factory Automation Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

10.3.1.5 Eastern Europe Industrial Control & Factory Automation Market Estimates and Forecasts, By Industry (2020-2032) (USD Billion)

10.3.1.6 Poland

10.3.1.6.1 Poland Industrial Control & Factory Automation Market Estimates and Forecasts, By Component Type (2020-2032) (USD Billion)

10.3.1.6.2 Poland Industrial Control & Factory Automation Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

10.3.1.6.3 Poland Industrial Control & Factory Automation Market Estimates and Forecasts, By Industry (2020-2032) (USD Billion)

10.3.1.7 Romania

10.3.1.7.1 Romania Industrial Control & Factory Automation Market Estimates and Forecasts, By Component Type (2020-2032) (USD Billion)

10.3.1.7.2 Romania Industrial Control & Factory Automation Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

10.3.1.7.3 Romania Industrial Control & Factory Automation Market Estimates and Forecasts, By Industry (2020-2032) (USD Billion)

10.3.1.8 Hungary

10.3.1.8.1 Hungary Industrial Control & Factory Automation Market Estimates and Forecasts, By Component Type (2020-2032) (USD Billion)

10.3.1.8.2 Hungary Industrial Control & Factory Automation Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

10.3.1.8.3 Hungary Industrial Control & Factory Automation Market Estimates and Forecasts, By Industry (2020-2032) (USD Billion)

10.3.1.9 Turkey

10.3.1.9.1 Turkey Industrial Control & Factory Automation Market Estimates and Forecasts, By Component Type (2020-2032) (USD Billion)

10.3.1.9.2 Turkey Industrial Control & Factory Automation Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

10.3.1.9.3 Turkey Industrial Control & Factory Automation Market Estimates and Forecasts, By Industry (2020-2032) (USD Billion)

10.3.1.10 Rest of Eastern Europe

10.3.1.10.1 Rest of Eastern Europe Industrial Control & Factory Automation Market Estimates and Forecasts, By Component Type (2020-2032) (USD Billion)

10.3.1.10.2 Rest of Eastern Europe Industrial Control & Factory Automation Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

10.3.1.10.3 Rest of Eastern Europe Industrial Control & Factory Automation Market Estimates and Forecasts, By Industry (2020-2032) (USD Billion)

10.3.2 Western Europe

10.3.2.1 Trends Analysis

10.3.2.2 Western Europe Industrial Control & Factory Automation Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

10.3.2.3 Western Europe Industrial Control & Factory Automation Market Estimates and Forecasts, By Component Type (2020-2032) (USD Billion)

10.3.2.4 Western Europe Industrial Control & Factory Automation Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

10.3.2.5 Western Europe Industrial Control & Factory Automation Market Estimates and Forecasts, By Industry (2020-2032) (USD Billion)

10.3.2.6 Germany

10.3.2.6.1 Germany Industrial Control & Factory Automation Market Estimates and Forecasts, By Component Type (2020-2032) (USD Billion)

10.3.2.6.2 Germany Industrial Control & Factory Automation Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

10.3.2.6.3 Germany Industrial Control & Factory Automation Market Estimates and Forecasts, By Industry (2020-2032) (USD Billion)

10.3.2.7 France

10.3.2.7.1 France Industrial Control & Factory Automation Market Estimates and Forecasts, By Component Type (2020-2032) (USD Billion)

10.3.2.7.2 France Industrial Control & Factory Automation Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

10.3.2.7.3 France Industrial Control & Factory Automation Market Estimates and Forecasts, By Industry (2020-2032) (USD Billion)

10.3.2.8 UK

10.3.2.8.1 UK Industrial Control & Factory Automation Market Estimates and Forecasts, By Component Type (2020-2032) (USD Billion)

10.3.2.8.2 UK Industrial Control & Factory Automation Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

10.3.2.8.3 UK Industrial Control & Factory Automation Market Estimates and Forecasts, By Industry (2020-2032) (USD Billion)

10.3.2.9 Italy

10.3.2.9.1 Italy Industrial Control & Factory Automation Market Estimates and Forecasts, By Component Type (2020-2032) (USD Billion)

10.3.2.9.2 Italy Industrial Control & Factory Automation Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

10.3.2.9.3 Italy Industrial Control & Factory Automation Market Estimates and Forecasts, By Industry (2020-2032) (USD Billion)

10.3.2.10 Spain

10.3.2.10.1 Spain Industrial Control & Factory Automation Market Estimates and Forecasts, By Component Type (2020-2032) (USD Billion)

10.3.2.10.2 Spain Industrial Control & Factory Automation Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

10.3.2.10.3 Spain Industrial Control & Factory Automation Market Estimates and Forecasts, By Industry (2020-2032) (USD Billion)

10.3.2.11 Netherlands

10.3.2.11.1 Netherlands Industrial Control & Factory Automation Market Estimates and Forecasts, By Component Type (2020-2032) (USD Billion)

10.3.2.11.2 Netherlands Industrial Control & Factory Automation Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

10.3.2.11.3 Netherlands Industrial Control & Factory Automation Market Estimates and Forecasts, By Industry (2020-2032) (USD Billion)

10.3.2.12 Switzerland

10.3.2.12.1 Switzerland Industrial Control & Factory Automation Market Estimates and Forecasts, By Component Type (2020-2032) (USD Billion)

10.3.2.12.2 Switzerland Industrial Control & Factory Automation Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

10.3.2.12.3 Switzerland Industrial Control & Factory Automation Market Estimates and Forecasts, By Industry (2020-2032) (USD Billion)

10.3.2.13 Austria

10.3.2.13.1 Austria Industrial Control & Factory Automation Market Estimates and Forecasts, By Component Type (2020-2032) (USD Billion)

10.3.2.13.2 Austria Industrial Control & Factory Automation Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

10.3.2.13.3 Austria Industrial Control & Factory Automation Market Estimates and Forecasts, By Industry (2020-2032) (USD Billion)

10.3.2.14 Rest of Western Europe

10.3.2.14.1 Rest of Western Europe Industrial Control & Factory Automation Market Estimates and Forecasts, By Component Type (2020-2032) (USD Billion)

10.3.2.14.2 Rest of Western Europe Industrial Control & Factory Automation Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

10.3.2.14.3 Rest of Western Europe Industrial Control & Factory Automation Market Estimates and Forecasts, By Industry (2020-2032) (USD Billion)

10.4 Asia-Pacific

10.4.1 Trends Analysis

10.4.2 Asia-Pacific Industrial Control & Factory Automation Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

10.4.3 Asia-Pacific Industrial Control & Factory Automation Market Estimates and Forecasts, By Component Type (2020-2032) (USD Billion)

10.4.4 Asia-Pacific Industrial Control & Factory Automation Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

10.4.5 Asia-Pacific Industrial Control & Factory Automation Market Estimates and Forecasts, By Industry (2020-2032) (USD Billion)

10.4.6 China

10.4.6.1 China Industrial Control & Factory Automation Market Estimates and Forecasts, By Component Type (2020-2032) (USD Billion)

10.4.6.2 China Industrial Control & Factory Automation Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

10.4.6.3 China Industrial Control & Factory Automation Market Estimates and Forecasts, By Industry (2020-2032) (USD Billion)

10.4.7 India

10.4.7.1 India Industrial Control & Factory Automation Market Estimates and Forecasts, By Component Type (2020-2032) (USD Billion)

10.4.7.2 India Industrial Control & Factory Automation Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

10.4.7.3 India Industrial Control & Factory Automation Market Estimates and Forecasts, By Industry (2020-2032) (USD Billion)

10.4.8 Japan

10.4.8.1 Japan Industrial Control & Factory Automation Market Estimates and Forecasts, By Component Type (2020-2032) (USD Billion)

10.4.8.2 Japan Industrial Control & Factory Automation Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

10.4.8.3 Japan Industrial Control & Factory Automation Market Estimates and Forecasts, By Industry (2020-2032) (USD Billion)

10.4.9 South Korea

10.4.9.1 South Korea Industrial Control & Factory Automation Market Estimates and Forecasts, By Component Type (2020-2032) (USD Billion)

10.4.9.2 South Korea Industrial Control & Factory Automation Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

10.4.9.3 South Korea Industrial Control & Factory Automation Market Estimates and Forecasts, By Industry (2020-2032) (USD Billion)

10.4.10 Vietnam

10.4.10.1 Vietnam Industrial Control & Factory Automation Market Estimates and Forecasts, By Component Type (2020-2032) (USD Billion)

10.4.10.2 Vietnam Industrial Control & Factory Automation Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

10.4.10.3 Vietnam Industrial Control & Factory Automation Market Estimates and Forecasts, By Industry (2020-2032) (USD Billion)

10.4.11 Singapore

10.4.11.1 Singapore Industrial Control & Factory Automation Market Estimates and Forecasts, By Component Type (2020-2032) (USD Billion)

10.4.11.2 Singapore Industrial Control & Factory Automation Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

10.4.11.3 Singapore Industrial Control & Factory Automation Market Estimates and Forecasts, By Industry (2020-2032) (USD Billion)

10.4.12 Australia

10.4.12.1 Australia Industrial Control & Factory Automation Market Estimates and Forecasts, By Component Type (2020-2032) (USD Billion)

10.4.12.2 Australia Industrial Control & Factory Automation Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

10.4.12.3 Australia Industrial Control & Factory Automation Market Estimates and Forecasts, By Industry (2020-2032) (USD Billion)

10.4.13 Rest of Asia-Pacific

10.4.13.1 Rest of Asia-Pacific Industrial Control & Factory Automation Market Estimates and Forecasts, By Component Type (2020-2032) (USD Billion)

10.4.13.2 Rest of Asia-Pacific Industrial Control & Factory Automation Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

10.4.13.3 Rest of Asia-Pacific Industrial Control & Factory Automation Market Estimates and Forecasts, By Industry (2020-2032) (USD Billion)

10.5 Middle East and Africa

10.5.1 Middle East

10.5.1.1 Trends Analysis

10.5.1.2 Middle East Industrial Control & Factory Automation Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

10.5.1.3 Middle East Industrial Control & Factory Automation Market Estimates and Forecasts, By Component Type (2020-2032) (USD Billion)

10.5.1.4 Middle East Industrial Control & Factory Automation Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

10.5.1.5 Middle East Industrial Control & Factory Automation Market Estimates and Forecasts, By Industry (2020-2032) (USD Billion)

10.5.1.6 UAE

10.5.1.6.1 UAE Industrial Control & Factory Automation Market Estimates and Forecasts, By Component Type (2020-2032) (USD Billion)

10.5.1.6.2 UAE Industrial Control & Factory Automation Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

10.5.1.6.3 UAE Industrial Control & Factory Automation Market Estimates and Forecasts, By Industry (2020-2032) (USD Billion)

10.5.1.7 Egypt

10.5.1.7.1 Egypt Industrial Control & Factory Automation Market Estimates and Forecasts, By Component Type (2020-2032) (USD Billion)

10.5.1.7.2 Egypt Industrial Control & Factory Automation Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

10.5.1.7.3 Egypt Industrial Control & Factory Automation Market Estimates and Forecasts, By Industry (2020-2032) (USD Billion)

10.5.1.8 Saudi Arabia

10.5.1.8.1 Saudi Arabia Industrial Control & Factory Automation Market Estimates and Forecasts, By Component Type (2020-2032) (USD Billion)

10.5.1.8.2 Saudi Arabia Industrial Control & Factory Automation Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

10.5.1.8.3 Saudi Arabia Industrial Control & Factory Automation Market Estimates and Forecasts, By Industry (2020-2032) (USD Billion)

10.5.1.9 Qatar

10.5.1.9.1 Qatar Industrial Control & Factory Automation Market Estimates and Forecasts, By Component Type (2020-2032) (USD Billion)

10.5.1.9.2 Qatar Industrial Control & Factory Automation Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

10.5.1.9.3 Qatar Industrial Control & Factory Automation Market Estimates and Forecasts, By Industry (2020-2032) (USD Billion)

10.5.1.10 Rest of Middle East

10.5.1.10.1 Rest of Middle East Industrial Control & Factory Automation Market Estimates and Forecasts, By Component Type (2020-2032) (USD Billion)

10.5.1.10.2 Rest of Middle East Industrial Control & Factory Automation Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

10.5.1.10.3 Rest of Middle East Industrial Control & Factory Automation Market Estimates and Forecasts, By Industry (2020-2032) (USD Billion)

10.5.2 Africa

10.5.2.1 Trends Analysis

10.5.2.2 Africa Industrial Control & Factory Automation Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

10.5.2.3 Africa Industrial Control & Factory Automation Market Estimates and Forecasts, By Component Type (2020-2032) (USD Billion)

10.5.2.4 Africa Industrial Control & Factory Automation Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

10.5.2.5 Africa Industrial Control & Factory Automation Market Estimates and Forecasts, By Industry (2020-2032) (USD Billion)

10.5.2.6 South Africa

10.5.2.6.1 South Africa Industrial Control & Factory Automation Market Estimates and Forecasts, By Component Type (2020-2032) (USD Billion)

10.5.2.6.2 South Africa Industrial Control & Factory Automation Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

10.5.2.6.3 South Africa Industrial Control & Factory Automation Market Estimates and Forecasts, By Industry (2020-2032) (USD Billion)

10.5.2.7 Nigeria

10.5.2.7.1 Nigeria Industrial Control & Factory Automation Market Estimates and Forecasts, By Component Type (2020-2032) (USD Billion)

10.5.2.7.2 Nigeria Industrial Control & Factory Automation Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

10.5.2.7.3 Nigeria Industrial Control & Factory Automation Market Estimates and Forecasts, By Industry (2020-2032) (USD Billion)

10.5.2.8 Rest of Africa

10.5.2.8.1 Rest of Africa Industrial Control & Factory Automation Market Estimates and Forecasts, By Component Type (2020-2032) (USD Billion)

10.5.2.8.2 Rest of Africa Industrial Control & Factory Automation Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

10.5.2.8.3 Rest of Africa Industrial Control & Factory Automation Market Estimates and Forecasts, By Industry (2020-2032) (USD Billion)

10.6 Latin America

10.6.1 Trends Analysis

10.6.2 Latin America Industrial Control & Factory Automation Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

10.6.3 Latin America Industrial Control & Factory Automation Market Estimates and Forecasts, By Component Type (2020-2032) (USD Billion)

10.6.4 Latin America Industrial Control & Factory Automation Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

10.6.5 Latin America Industrial Control & Factory Automation Market Estimates and Forecasts, By Industry (2020-2032) (USD Billion)

10.6.6 Brazil

10.6.6.1 Brazil Industrial Control & Factory Automation Market Estimates and Forecasts, By Component Type (2020-2032) (USD Billion)

10.6.6.2 Brazil Industrial Control & Factory Automation Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

10.6.6.3 Brazil Industrial Control & Factory Automation Market Estimates and Forecasts, By Industry (2020-2032) (USD Billion)

10.6.7 Argentina

10.6.7.1 Argentina Industrial Control & Factory Automation Market Estimates and Forecasts, By Component Type (2020-2032) (USD Billion)

10.6.7.2 Argentina Industrial Control & Factory Automation Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

10.6.7.3 Argentina Industrial Control & Factory Automation Market Estimates and Forecasts, By Industry (2020-2032) (USD Billion)

10.6.8 Colombia

10.6.8.1 Colombia Industrial Control & Factory Automation Market Estimates and Forecasts, By Component Type (2020-2032) (USD Billion)

10.6.8.2 Colombia Industrial Control & Factory Automation Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

10.6.8.3 Colombia Industrial Control & Factory Automation Market Estimates and Forecasts, By Industry (2020-2032) (USD Billion)

10.6.9 Rest of Latin America

10.6.9.1 Rest of Latin America Industrial Control & Factory Automation Market Estimates and Forecasts, By Component Type (2020-2032) (USD Billion)

10.6.9.2 Rest of Latin America Industrial Control & Factory Automation Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

10.6.9.3 Rest of Latin America Industrial Control & Factory Automation Market Estimates and Forecasts, By Industry (2020-2032) (USD Billion)

11. Company Profiles

11.1 Yokogawa Electric Corporation

11.1.1 Company Overview

11.1.2 Financial

11.1.3 Products/ Services Offered

11.1.4 SWOT Analysis

11.2 Omron Corporation

11.2.1 Company Overview

11.2.2 Financial

11.2.3 Products/ Services Offered

11.2.4 SWOT Analysis

11.3 WIKA

11.3.1 Company Overview

11.3.2 Financial

11.3.3 Products/ Services Offered

11.3.4 SWOT Analysis

11.4 Mitsubishi Electric Corporation

11.4.1 Company Overview

11.4.2 Financial

11.4.3 Products/ Services Offered

11.4.4 SWOT Analysis

11.5 Rockwell Automation

11.5.1 Company Overview

11.5.2 Financial

11.5.3 Products/ Services Offered

11.5.4 SWOT Analysis

11.6 Yaskawa Electric Corporation

11.6.1 Company Overview

11.6.2 Financial

11.6.3 Products/ Services Offered

11.6.4 SWOT Analysis

11.7 Toshiba Corporation

11.7.1 Company Overview

11.7.2 Financial

11.7.3 Products/ Services Offered

11.7.4 SWOT Analysis

11.8 Honeywell International Inc.

11.8.1 Company Overview

11.8.2 Financial

11.8.3 Products/ Services Offered

11.8.4 SWOT Analysis

11.9 Dwyer Instruments

11.9.1 Company Overview

11.9.2 Financial

11.9.3 Products/ Services Offered

11.9.4 SWOT Analysis

11.10 Stratasys

11.10.1 Company Overview

11.10.2 Financial

11.10.3 Products/ Services Offered

11.10.4 SWOT Analysis

12. Use Cases and Best Practices

13. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

Key Segmentation

By Component Type

Industrial Robots

Collaborative Industrial Robots

Machine Vision

Control Valves

Field Instruments

Human–Machine Interface (HMI)

Industrial PC

Sensors

By Solution

SCADA

PLC

DCS

MES

Industrial Safety

PAM

By Industry

Process Industry

Oil & GAS

Chemical

Pulp & Paper

Pharmaceutical

Metals & mining

Food & Beverages

Energy & Power

Discrete Industry

Automotive

Machine manufacturing

Semiconductor & Electronics

Aerospace & Defense

Medical device

Request for Segment Customization as per your Business Requirement: Segment Customization Request

Regional Coverage

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of the Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Rest of Latin America

Request for Country Level Research Report: Country Level Customization Request

Available Customization

With the given market data, SNS Insider offers customization as per the company’s specific needs. The following customization options are available for the report:

Product Analysis

Criss-Cross segment analysis (e.g. Product X Application)

Product Matrix which gives a detailed comparison of product portfolio of each company

Geographic Analysis

Additional countries in any of the regions

Company Information

Detailed analysis and profiling of additional market players (Up to five)

The Automatic Labeling Machine Market size was estimated at USD 3.04 billion in 2023 and is expected to reach USD 4.25 billion by 2032 with a growing CAGR of 3.82% during the forecast period of 2024-2032.

North America Electrostatic Precipitator Market size was estimated at $1.40 Bn in 2023 and will reach $2.10 Bn by 2032 at a CAGR of 4.62% by 2024-2032.

The Industrial Air Filtration Market size was valued at USD 7.33 Billion in 2023 and is expected to reach USD 12.83 Billion by 2032 and grow at a CAGR of 6.42% over the forecast period 2024-2032.

The Countertop Market size was valued at USD 131.2 Billion in 2023 and is now anticipated to grow to USD 233.2 Billion by 2032, displaying a compound annual growth rate of 6.6% during the forecast Period 2024-2032.

The Lawn & Garden Equipment Market size was valued at USD 27.90 Billion in 2023 and is now anticipated to grow to USD 54.39 Billion by 2032, displaying a compound annual growth rate (CAGR) of 7.7% during the forecast Period 2024 - 2032.

The Palletizer Market size was USD 2.77 billion in 2023 and is expected to Reach USD 4.05 billion by 2032 and grow at a CAGR of 4.32% over the forecast period of 2024-2032.

Hi! Click one of our member below to chat on Phone

© 2024 All Rights Reserved by SNS Insider Pvt Ltd